Fidinam: Which housing arrangements can reduce your taxable income?

You are residing in Hong Kong. As an employee, you receive a salary, a substantial part of which is allocated to pay your rent. Did you know that by asking your employer to provide you with rent-free or subsidized accommodation, you could reduce your income subject to Salaries Tax?

There are three ways employers can grant employees housing support:

- Housing Allowance: The employer grants the employee extra cash, included within his salary, having no control on how the employee will spend the money.

- Rent-Free Accommodation: The employer, as a company, rents a flat and provides it to his employee as place of residence (in which case the lease agreement is entered into with the employer). In such case, the employer automatically controls the rental spending.

- Subsidized Accommodation: The employer wholly or partially reimburses the rent paid by the employee (in which case the lease agreement is entered into by the employee), and proper supervision is exercised over the employee’s expenditures.

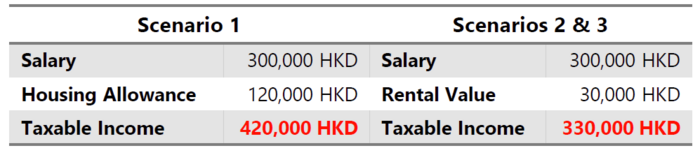

Under scenario 1, and since the employer has no proper control over the expenditures of the employee, the full amount of the Housing Allowance is treated as salary, and is therefore be subject to Salaries Tax.

Under scenarios 2 and 3, and as long as the employer exercises a proper degree of control over the employee’s expenses, the Inland Revenue Ordinance (“IRO”) only treats the “Rental Value” of the flat as taxable income, instead of taxing the employee on the actual amount of rent paid or reimbursed by the employer. This is very advantageous to the employee, as the Rental Value is computed at the standard rate of 10% of the employee’s total remaining income.

By reducing your assessable income, you automatically reduce the amount of Salaries Tax payable, regardless the progressive rates applying to your situation.

The grant is neutral for employers, while it enables employees to reduce their tax exposure. Ask for it!